Data driven decisions help get wins

“We are card counters at the blackjack table. And we’re gonna turn the odds on the casino:” Billy Beane in the movie Moneyball. “Strategically Transforming the Mortgage Banking Industry” profiled Oakland Athletics General Manager Beane and his data-driven approach to winning baseball games at a low cost per win. Beane’s big data approach brought about a strategic shift in baseball. The shift occurred from a subjective, “can’t quite put your finger on it” player selection to a data driven approach described in Michael Lewis’ book, ‘Moneyball’.

“Your goal shouldn’t be to buy players. Your goal should be to buy wins. In order to buy wins, you need to buy runs:” Peter Brand in the movie Moneyball. Mr. Beane is an exemplar of the innovative use of data within a business. And baseball is a business. It is compensation heavy, meaning much of the cost of the product is wages, similar to mortgage banking. And it has its star players, much the same as the highly compensated ‘heavy hitter’ mortgage originator.

Beane’s question, “How do we win games at the lowest cost per win?” The traditional scouting paradigm looks at the five tools of baseball: speed, power, hitting for average, fielding and arm strength. These tools appear to be measurable as inputs. But do the inputs produce the desired output? Wins, and at what cost?

Beane correlated the metrics that win games with the cost of the players earning the wins. He found it possible to consistently have one of the lowest costs per win in major league baseball. Beane did so by paying close attention to data driven decision making to find players that were not valued for the skills that win games at the lowest cost per win.

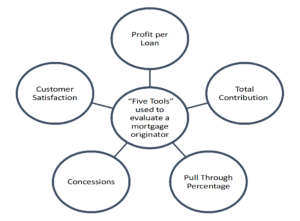

What are the “Five Tools” used to evaluate a mortgage originator?

Notice how volume is not listed.

Volume is rarely well correlated to profitability of a loan officer or a branch. The “Five Tools” of a mortgage originator are well correlated to profitability. It’s just that the data to measure them is buried in various systems and is not easily accessible and often requires association of data from disparate systems and data sources.

The effort to develop the “Five Tools” to measure loan officer and branch performance is well worth it. How do I know? I often ask CEOs, “Who are your top ten producers?” Their answers are usually based on volume, and volume mix. Their answers rarely correlate with the top 10 most profitable producers based on the “Five Tools of Mortgage Origination”.

“If we pull this off, we change the game. We change the game for good:” Billy Beane in the movie. Profit per loan, total contribution margin per month, pull through percentage, concessions and customer satisfaction work hand in hand to identify the most profitable originators. The “Five Tools” best identify lender profitability in loan origination.